My Top 10 Ideas As Of End of January 2024

Disclaimer: Not investment advice. Do your own research. For informational purposes only. I reserve the right to change positions after publishing as events change. Position rankings are accurate as of 1/31/24.

Last time I sent an email it was on 1/1/24: “My Favorite Biotech Ideas For 2024” and I listed 12 public companies that I was focused on for the new year. After a month of reflection and news flow, I have been making some tweaks.

When I update the 2024 post on 1/1/2025 don’t worry I’ll still use the original companies (no cheating) but I thought an update a month later would be prudent. I now think five of the 12 companies I listed below might take until 2025 to fully inflect, while I have added three companies not listed into my Top 10 positions. Below I’ll list my 10 favorite ideas in order. I was always a fan of David Letterman’s Top Ten list so I thought that would be a fun monthly concept.

But first to jog your memory here was the list from 1/1/2024, with prices as of 1/31/24 close:

Names you won’t find below: ARQT, PHAT, VRNA, GOSS, LYRA. Why? Well the common thread with all five is I feel I was too early to the story compared to other more near-term opportunities.

ARQT launched their foam at the start of 2024 and Dermatology launches are just slower and heavier lifts than I probably originally acknowledged. Plus the stock recently went up like 85% in just a couple weeks and it seems prudent to take profits here as the calculus has changed dramatically.

Same launch concerns with PHAT who is launching a new class that competes with PPIs, a heavily generic class. They have a superior drug but I think it will take more time than I would have liked to believe to gain traction there, although the first earnings report post launch should be interesting.

VRNA won’t be approved until June at the earliest so I doubt the launch takes off in a meaningful way before 2025 although they could attract acquirer interest. I think it’s a very compelling new mechanism but the stock just kind of drifts sideways plus being long into a PDUFA date is risky lately.

GOSS won’t have data until 2025 and I probably overrated their business development prospects before that data. There doesn’t seem to be a lot of movement or interest currently, although that could change.

LYRA has a Phase 3 this year but will need another positive Phase 3 in 2025 so that’s an overhang on the stock and I’m not sure the first Phase 3 will be anything other than a chance to execute an offering.

I’m still interested in all of those companies for the record. I just feel I’m early outside of ARQT which is really on a very surprising run and is now probably fairly valued for now. I have three new names to add below to round out a Top Ten.

My Current Top 10, By Position Size

#1: Cullinan Oncology (CGEM)

This is my #1 position for a number of reasons. Six programs in the clinic, excellent management, and trading roughly close to cash as I write this. (Editor note: It rallied fairly hard over the last week.) But most of all is the catalyst map that will begin playing out starting in June. I think one of the reasons the company dipped below cash is because they were in a “catalyst desert” with nothing to talk about except IND clearances and Phase 1 starts. That won’t be the case going forward. Their lead program, CLN-619, will have first combination data in addition to more monotherapy data in June. What I like about CLN-619 is it is a first-in-class asset with monotherapy activity in a relatively uncluttered indication of 2L endometrial cancer:

The mechanism of a MICA/B antibody (preventing MICA/B cleavage and enhancing T cell, NK cell, and macrophage binding) should pair well with PD-1 inhibition. The agent appears safe allowing for double and perhaps even triple combos down the road. I don’t understand why their monotherapy data hasn’t gotten more eyeballs but future data updates should be more noticed if the thesis plays out like I think it will.

Their second pipeline asset, zipalertinib (partnered 50/50 with Taiho with $130m in outstanding milestones) is in Phase 2b and Phase 3 trials currently. There won’t be catalysts in 2024 aside from enrollment updates but I’m researching the exon20 NSCLC space for a future email. If nothing else I expect this agent to be competitive taking at least 50% of a modestly sized market and providing milestone payments and non-dilutive capital and a royalty stream.

Two other assets, CLN-049 a FLT3xCD3 T-cell engager for AML and CLN-418 a B7H4x4-1bb bispecific immune activator testing in multiple solid tumors, will have Phase 1 data in 2024. There is a fifth asset, CLN-978 a CD19xCD3 T-cell engager that is seemingly pivoting to treatment of autoimmune disorders and should have Phase 1 data in B-cell NHL in early 2025. I would encourage everyone to listen to the JPM presentation for more in-depth discussion about the opportunity for CLN-978 specifically in autoimmune disease.

A sixth (!) clinical asset exists, CLN-617 a collagen-binding IL-12 and IL-2 fusion protein, and should also have data in 2025. Is it too much? I don’t think so. The sooner they can get all these assets to proof-of-concept the sooner they can find what they have. Due to the laws of biotech, not all six will be compelling. I assume CLN-619 will stay full owned. Possibly CLN-418 since it might be synergistic with CLN-619. Everything else is up for partnership or sale. CLN-978 for autoimmune diseases seems incredibly valuable now that every company is pivoting into cell therapy for SLE but I’m not sure yet if the company would be better served by partnering it or expanding their focus beyond oncology. Good problems to have at least.

I think Cullinan Oncology has a lot of ways to drive value and the valuation seems incredibly reasonable to me even though the stock has been on a mini run over the last few months. I think once we hit June the company will have so many things in the clinic that major stock moving data sets should happen every couple of months.

#2: Edgewise Therapeutics (EWTX)

This is a company not on my previous 2024 list. This is another investment where I feel there are multiple ways to win. First, I have to admit I got lucky. After staking out the company based on the tweets of @dedwng I notice the company was dipping hard to the $9/share level. My dream buy price was in the 7s but with everything else rallying I took a rather large position anyway figuring I might not get a better chance and I needed to deploy some cash. The next week I received an unexpected break because the company announced a private placement with high quality biotech hedge funds that priced above market. The stock has rallied 50% on that news and I suspect the funds are interested in EDG-7500 for hypertrophic cardiomyopathy.

But first I want to talk about EDG-5506 their drug for Becker Muscular Dystrophy (“BMD”) and Duchenne Muscular Dystrophy (“DMD”) post gene therapy. Very few investors seem to be giving the company credit for these programs. And I understand neither indication has placebo-controlled data and musclar dystrophies are hard indications which to develop new therapies. But I find the selection of BMD to be an interesting, uncrowded indication for a fast myofiber myosin inhibitor and the open label data so far seems markedly better than natural history which has been established by two different methodologies.

EDG-5506 will have its first placebo-controlled data in Q4 but before that there will be a 24 month open label data update. If the 12 patients above remain, on average, as stable at 24 months or minimally declined I think that’s a huge derisking event for the Q4 placebo-controlled Phase 2 data which could even qualify the company for accelerated approval depending on the strength of the data. And their “Grand Canyon” Phase 3 trial should reach full enrollment soon.

BMD is a potential blockbuster indication (12,000 patients, significant morbidity, no approved agents) and also DMD post Gene Therapy presents very similar to BMD (watch JPM presentation for more detail) and could be an even larger blockbuster indication. I will be keenly watching the EDG-5506 update in 1H 2024 to see what clues there are to future probability of success.

But as I mentioned I think the real run in the stock is based on EDG-7500 which actually evolved as a compound they found from a counter-screen of EDG-5506 to determine skeletal muscle vs. cardiac muscle selectivity. EDG-7500 is targeting the large market of hypertrophic cardiomyopathy. It doesn’t even have Phase 1 data yet but the rationale and pre-clinical work is intriguing. With Myokardia ($13 billion acquisition) and Cytokinetics (potential $10 billion+ acquisition) in the news it’s not hard to see why funds would be attracted to a $1 billion company that could leapfrog both of those assets years down the road. A good way of hedging their bets in CYTK at least and good for Edgewise as they now have enough cash to see all their currently planned trials through to completion.

#3: Alpine Immune Sciences (ALPN)

Thankfully I don’t have to write too deeply on my thesis here. I think they have a best-in-class BAFF/APRIL inhibitor with excellent safety and room to dose up even if needed. They only have data in 6 patients across two indications but it looks incredible so far. I believe the two indications, IGa Nephropathy and Primary Membranous Nephropathy, are best served by BAFF/APRIL inhibition compared to other modalities and combined are 400,000 patients in the G8 countries.

Two recent expert calls on Slingshot Insights (one led by me, one not, both require purchase) were extremely positive on the early data, although with the caveat it is very early in clinical development. More de-risking data is coming all through 2024. If this is clearly a best-in-class asset then the ceiling for it is a mega blockbuster and much much higher from here. I’m keeping it simple and this as one of my bigger positions.

#4: Delcath Systems (DCTH)

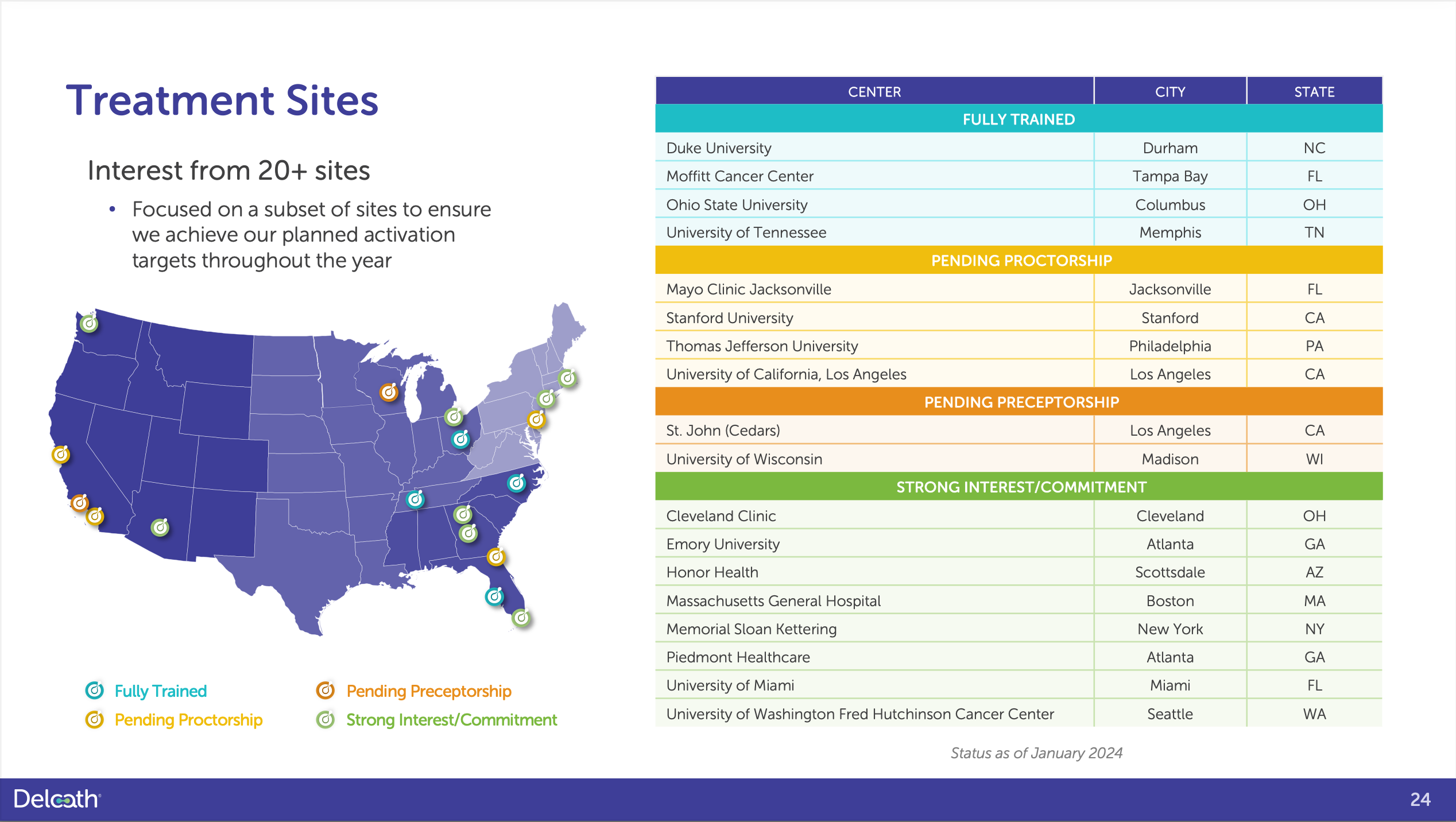

This is a company not on my previous 2024 list. I originally omitted it because I thought it was going to be a 2025 story. I have now changed my thesis based on a few very recent events. First, the company announced their commercial launch of Hepzato to treat metastatic uveal melanoma and the first site to launch has announced they will be treating five patients in January. This is a very expensive drug/device combination. Even the minimum first two treatments combined cost $365,000 total and most patients get an average of 4 treatments spaced out every 6 to 8 weeks. So a primary investigator publicly tweeting about treating five commercial patients starting in January which would be $1.5 million+ in revenue from one treatment site in one month alone. The company’s cash operating expenses are only $10 million per quarter.

Next, I re-read their last earnings call and reviewed their newest corporate deck. Their November earnings call said their goals were having 5 centers in Q1 doing 1 treatment per month, 10 centers in Q2, and 15 centers by the end of the year doing two per month. However later in the call they remarked that 5 centers should be up by the “end of January” alluding to a faster timeline. Then when their new corporate presentation came out during JPM week, four centers were listed as fully trained, four more high volume centers were awaiting proctorship (the last step), and two more were awaiting preceptorship. So it seems like 10 centers will definitely be treating patients in the near future and they are ten of the highest volume mUM centers in the country.

The one treatment per month thing seems like a classic sandbagging of expectations to overdeliver after so many delays in the past with regulatory issues out of their control. I think one treatment per week is reasonable by end of year for most of these 10 centers at the top of the above image. Word should spread fast about this treatment option especially for patients that aren’t eligible for KIMMTRACK or 2L patients.

Finally, the estimates are simply too low. Bloomberg estimates have Delcath selling less than $8 million in Q4 2024. Even the direct company guidance from that November earnings call would correlate with $16 million in sales by Q4 (15 centers x $1.1 million in sales each). I think they will do that in Q2. I mean, even Q1 is not completely out of the question if the volume per center is one treatment per week…

With a limited share count of 28.6 million outstanding (plus 7.8m warrants and 4.1m stock options) and even if you were to assume every warrant and option was exercised PLUS if they did a 9.5m share offering on top of that for more cash towards label expansion studies, that’s still only 50 million shares outstanding for a product with a peak sales potential of $500 million in mUM alone. Plus there is potential to be tapped in other liver-dominant cancers that might be ripe for a partnership or sale.

#5: Avadel (AVDL)

The first two full quarters of Avadel’s once nightly narcolepsy drug Lumryz have been excellent but it doesn’t feel the market has truly appreciated how hot they have come out of the gate. At the end of Q3, the first full quarter of launch they had 1,000 patients enrolled in their patient assistance program and 400 on commercial therapy. Recently, they reported at the end of Q4 they had 1,900 patients in the assistance program and 1,000 on therapy.

Patients in most cases need to titrate this medication up so patients likely aren’t on the full dose yet but when they are the company anticipates the average dose will be 7.5mg nightly with a net pricing of $120,000 annually. If even the current 1,900 patients in the assistance program convert to therapy at $30,000 net pricing per quarter that’s $57 million in revenue per quarter. That’s just for patients already in the pipeline to get on commercial therapy. And we know the company won’t be stagnant and will continue to add new switch patients, previously treated oxybate patients who discontinued because of the twice nightly profile of the Jazz pharmaceuticals products, and oxybate naive patients.

My belief is the oxybate market will eventually grow to 25,000 patients in Narcolepsy (adults and pediatric, from ~16,000 now) fueled by Lumryz’s improved product profile compared to the Jazz offerings and another 25,000 patients in Idiopathic Hypersomnia once they get approval in that indication. 50,000 patients at $120,000 net pricing annually (assuming average dose of 7.5mg nightly and gross to net discounts stay flat) is a $6 billion market that I expect Avadel to take >50% of in the next five years. Patient and provider surveys show over 50% preference for the once nightly product despite containing higher salt amounts.

The holy grail in this space would be a once nightly, no/low salt product that would marry the best attributes of both the newest Avadel and Jazz offerings. I don’t know who will get there first but I’m inclined to guess Avadel in that Jazz could not crack the once nightly PK puzzle for so long and aggressively invested in a now discontinued Orexin-2 receptor agonist that was halted due to safety concerns. If they were close on a once nightly, no/low salt formulation I think their business development strategy would have looked different.

Avadel is already telegraphing they will pursue this path with their existing long-acting technology and if they don’t get there I feel the once nightly advantage is far greater than the low sodium advantage and they have intellectual property protection out until 2042. The stock might look expensive at over a billion dollars but considering how soon they might be approaching blockbuster sales, I think there is plenty of upside left.

The next five companies rely on more binary outcomes, hence are riskier and smaller positions for now:

#6: G1 Therapeutics (GTHX)

This is a new company not on my previous 2024 list. G1 has an approved product, Cosela (trilaciclib) a CDK4/6 inhibitor that improves tolerability of chemotherapy with Extensive Stage Small-Cell Lung Cancer. Sales were roughly ~$13 million in Q4 2023 and are growing decently after a rough launch and some drug shortage issues with platinum-based chemotherapy used in ES-SCLC. The company fell as low as a $60 million valuation when it seemed like between the drug shortage and some clinical trial failures that they were headed for a pretty rough future.

In the last few months, things have changed somewhat. Their JPM presentation was actually full of new information not previously known that changed the story in a substantial way. In fact I counted five new pieces of information:

The platinum-based chemotherapy drug shortage has alleviated and GTHX had 19% QoQ volume growth

The company is doing a “Phase 4” overall survival trial in ES-SCLC, likely in response to the slow launch of Cosela and that improving patient safety might not be sufficient to drive full uptake in the $700m ES-SCLC market

New subgroup analysis from the company’s Phase 2 trial in Triple Negative Breast Cancer showed robustness across a variety of different analyses

A Phase 2 trial in TNBC in combination with ADCs showed an improvement in overall survival in the Cosela arm, compared to an earlier cut of the data where the survival looked WORSE in the Cosela arm (possibly a fluky artifact but very troubling at a time where a mCRC Phase 3 had just failed)

Through a variety of business development deals and reduced expenses, the company has extended their cash runway into 2025

In the near term, the interim analysis for the overall survival Phase 3 in TNBC is a huge data event. The interim analysis is powered for an earlier stop to the trial at a hazard ratio of 0.61 and the previous Phase 2 trial showed a HR of 0.31 in the dosing regimen that went forward in the Phase 3. However, with a median OS of 12.6 I think you could argue that maybe the control arm underperformed slightly. Still, even with an expected overall survival of 14-15 months in the control arm I would argue that the trial with 174 patients seems 50/50 to succeed if the drug arm from Group 2 has an overall survival of greater than 18 months depending on the shape of the curve. Management seems to be strongly hinting they think there is a chance of an early stoppage…HR=0.61 is a high bar and I’m worried if the trial continues to the full endpoint (expected late 2024) the stock reaction will be negative even if the trial could still work. And the stock has quadrupled almost since the nadir last October when the stock barely held $1/share. Now it’s roughly $4 so the risk/reward is different.

But the reason to be bullish is that the company has constrained expenses to a high degree, is ramping ES-SCLC sales with investigator-led survival data in ES-SCLC that may push things forward in the interim, TNBC has a shot at success, the Phase 4 ES-SCLC data could come in a few years, TNBC + ES-SCLC combined are over a billion dollars in addressable market, and with patent term extensions they will have exclusivity until at least 2034. There is big commercial operating leverage possible here if the TNBC trial works.

Is the TNBC Phase 3 trial completely a binary event? No, not completely. They still have the approval and sales in ES-SCLC that are annualizing close to $60 million/year with a chance of peak sales of $400 million if they capture > 50% of the market. But achieving those sales will require success in a overall survival trial for ES-SCLC which seems unlikely to work if even the strong TNBC Phase 2 OS data was a false positive. We still don’t know why exactly the mCRC trial failed, although there are some theories. And failure in TNBC would harm the company’s ability to raise further capital on good terms to extend beyond 2025. They would need to get to profitability fast to control their own destiny or just sell the company in a fire sale situation.

So the interim analysis is highly layered but one with high upside. Success in a overall survival trial in TNBC might even give ES-SCLC doctors confidence that recent investigator-sponsored data showing increased survival is a real signal and boost sales even before the 2027 readout of their company-sponsored survival study. (Here is the listing for the company’s own “Phase 4” survival trial.)

#7: Fulcrum Therapeutics (FULC)

I have written about this in my book, in past emails, so I’m not sure what to say at this point. If anything studying EWTX emboldens my confidence because the natural history of FSHD (showing -7.5% yearly decline) is tracking very, very similar to BMD. But FULC actually has placebo controlled data from Phase 2 showing stabilization and improvement, received an excellent accommodation from FDA/EMA on the primary endpoint, and FSHD is a 2x-3x larger indication globally than BMD. I assign the SCD program no value. It’s all in on the October catalyst but it can be sized a little smaller than other positions because the upside is so massive if it works.

#8: Fusion Pharmaceuticals (FUSN)

If the first company-sponsored Phase 2 data in mCRPC is well received in April, I don’t expect it to remain a stand-alone pure play radiopharmaceuticals company for long and my (wild) guess is AstraZeneca tries to acquire it since they have an existing partnership with the company. I owned a lot of this at one point but reduced my exposure as the stock has quadrupled from the lows. But it’s been such a good performer it’s hard to let it go completely. And I love this space and I do believe the mCRPC market will be massive and eventually move to Actinium therapies if safe. I think I have sold more than half of my peak allocation so I’m content to let the rest ride as of now but if it keeps going up it would be tempting to lighten up even more as the April data is fairly binary. They need compelling efficacy data plus have guided to very few if any Grade 3 adverse events in certain categories. That’s a high bar. But if they succeed I’d imagine there would be huge strategic interest here. And how many unencumbered radiopharmaceutical assets are left? Not many.

#9: Glycomimetics (GLYC)

I wrote about GLYC before but Phase 3 AML data coming up: AML is a graveyard indication of drug development, no placebo-controlled data, and the stock is up quite a bit on the year changing the calculus. My buys were around $1 and now it’s $3 which makes it very hard to hold into a huge binary. But I can’t let this little baby go completely as I do think maybe it’s crazy enough to work. But if it keeps rallying before the Q2 data I’m not sure in good conscience what position I can continue to hold, full disclosure. This was a great opportunistic buy, the kind I should have made on G1 Therapeutics in size when it fell to a dollar. The question remains: Why is this overall survival trial taking so damn long to complete? Is the drug having miracle effects or is this just the weirdest fluke of control arm outperformance ever? On a nerd level, I’m excited to see the answers at least. Let’s see that data!

#10: Coherus (CHRS)

MY PERSONAL OPINION AND HOT TAKE TIME: This company is run by an ineffective CEO. He should be relieved of his professional duties. The CCO should be the interim CEO and an exhaustive search for a new CEO should begin immediately. Enough is enough. The recent asset sale was a very bad idea. I sold my shares purchased around $2 when the stock popped at the open and vowed to never return, ever. I wanted to take my small profit and run away from this company that I have followed for years and traded with various degrees of success (or failure).

A few days later I bought a small position just so I could list this at #10 and talk about it. Because I’m a glutton for punishment I guess. This CEO is obsessed with transforming into an immuno-oncology company and selling their other assets for pennies on the dollar. They are being very clear about that. Caveat emptor.

WITH ALL THAT SAID…

There is still a lot of value from Udenyca’s on-body injector if that product can launch with no legal challenges. The stock has declined to a point where it might look attractive to some. With a very small position, I am in watch and wait mode. Frankly, this guy drives me up a wall… I’m not even going to say his name.

In fact, I’m tired of talking about the company! If they can squeeze the full value out of Udenyca and Loqtorzi story, which combined should be able to achieve sales of close to a billion dollars, the stock could do really well. I currently don’t expect that to happen based on CEO track record. But I would LOVE to be wrong and move this up the Top Ten rankings.

Okay screw it I’ll say his name: Dennis Lanfear, make me eat my words! This is a challenge! Show me you can create shareholder value and take this stock to all-time highs! (That’s >$22.34/share by the way. You are at $2.15) If so, I will issue you a very public apology in this newsletter all about how you are smart and I am stupid. I would love nothing more. You are sitting on two compelling assets in Udenyca and Loqtorzi. Sell Yusimry already and let’s get this show on the road!

No. More. Excuses. EXECUTE!

That’s it for now! I should have another post in a few weeks to a month either with some updates on commercial launches or a post on March 1st with an update to the Top Ten.

Until then,

Matt

Hi Matt,

Phathom Pharma (PHAT) is taking on 320 sales staff to promote Voquezna this year:

https://investors.phathompharma.com/static-files/05e1d7fe-b638-488b-b01a-88764b862d10

They claim to have enough funds for operations until 2026.

Was wondering if there is a more efficient method to reach health care professionals other than having this huge salesforce?

Hi Matt, thank you for your post and sharing your insights--very enlightening and informative. I am long 6/10 from your current top 10.

As for CHRS, I was surprised at the Cimerli divestment as well, but I'm not sure it was such a terrible idea.

Including the ones already approved, I believe there are around 10 ranibizumab biosimilars in development. I don't know how long Cimerli could have continued its current growth trajectory while maintaing favorable margins. Add to that several new promising drugs currently in development for the same indications.

Yusimry economics are different, though I wouldn't be surprised if they eventually divest Yusimry as well. As for Udenyca, since it overlaps with their growing oncology franchise--I think it might make more sense from a strategic viewpoint.

I think the generics/biosimilar business is tough unless one can operate at scale and leverage the sales org across multiple assets. The Cimerli deal helps them start to rightsize the balance sheet--while continuing to grow higher margin revenue to replace revenue lost from Cimerli. Anyway, jmtc.