My Top 10 Ideas As Of End of March 2024, Part 2

Disclaimer: Not investment advice. Do your own research. For informational purposes only. I reserve the right to change positions after publishing as events change. Position rankings are accurate as of pre-market 3/25/24 when writing was completed.

This is the second part of yesterday’s post!

To summarize Part 1:

#1: CELC, #2: EWTX, #3: FULC, #4: CGEM, #5: AVTE

My Current Top 10 Biotech Positions, By $ Value

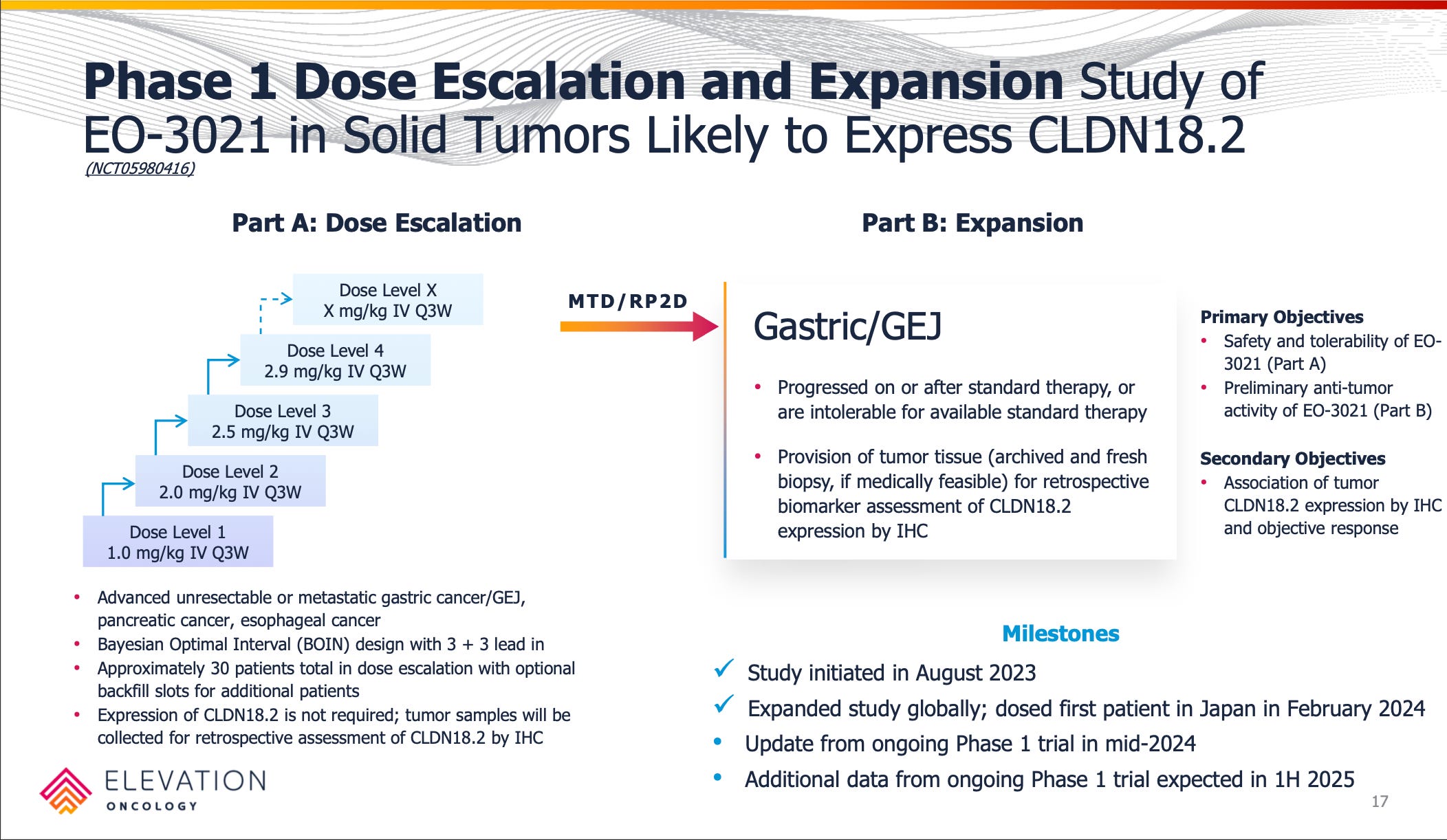

#6: Elevation Oncology (ELEV) [Last Month: NR, ⭐️]

Other people have written this up more in-depth on Twitter so I’ll just summarize what I have learned from them: Claudin18.2 is a validated oncology target from naked antibody data and CAR-T data, ADCs are the best modality to reach the entire spectrum of Claudin 18.2 expressing cancers including low expressing cancers (and ADCs are eating the entire oncology space in general due to outstanding efficacy), only two ADCs (ELEV and AstraZeneca) are in the clinic AND have produced data so these two programs probably have a 12 to 18 month head start on the competition, site specific conjugation of the Elevation Oncology ADC allows a potentially best-in-class safety profile which could allow for combination treatments, pre-treating for nausea and vomiting should allow for higher dosing than already seen in the initial data cut from Elevation’s Chinese partner (who they in-licensed the drug from), 45%+ response rate in gastric cancer is incredible and if they increase the dose further and reduce the rates of nausea/vomiting the product profile will be even better.

I mean look at that data and that’s with most patients at 2mg/kg! Only two gastric cancer patients at 2.5mg/kg. The DLTs started at 3mg/kg but with Elevation smartly pre-treating for nausea and vomiting I really like this dose escalation strategy below…basically see if you can get to 2.9mg/kg in multiple patients with no DLTs and then keep pushing slowly from there until the ADC hits the maximum of what it is capable of, in line with the FDA’s Project Optimus guidelines.

The gastric market is fulsome with 26,000 patients needing much better therapies and a vast majority of them having at least some Claudin18.2 expression. (10% of tumor cells expressing CLDN18.2, 1+ IHC staining intensity.) Notably, Elevation is not pre-screening for Claudin18.2 expression in their dose escalation study and is treating all comers which I think is a smart strategy competitively to show they can show best-in-class efficacy while addressing all patients. Plus, we don’t know just how little Claudin 18.2 expression one needs to show a possible response. Biomarker data will give some clues but if this could work well for the majority of gastric patients without the need for staining or other factors that could complicate patient identification and constrain a launch.

I like that they are laser focused on gastric cancer only after this initial dose escalation and also have Japanese clinical sites open (where there is higher incidence of gastric cancer) for faster enrollment. The company seems intent on getting this to patients as fast as possible and not squandering their lead and I’m interested to see what trial design they come with for registrational studies. Perhaps an adaptive Phase 2/3 with AA potential? We’ll see.

#7: Chimerix (CMRX) [Last Month: NR, ⭐️]

Chimerix is a true “fallen angel” from a valuation perspective but I think there could be value here. It is trading like absolute crap for reasons I can’t quite figure out why because it feels like the data produced thus far does not deserve this extreme discount.

Chimerix has a ~ $90m Market Cap (as of writing time and with its recent stock plunge), $193m in shareholder equity, quarterly burn of less than $16m per quarter, with a Phase 3 interim analysis in 2025 (albeit with a high bar for success) and full Phase 3 data in 2026. They are enrolling now for potential approval in H3 K27M glioma, an extremely tough indication with no approved therapies. I understand the market thinking the chances of success are low but at this depressed valuation with possible peak sales > $400m even if you think the probability of success is only a few percent this still should be trading higher into data in my opinion. (I personally would put the probability of success anywhere from 10%-30% depending on the day but I’m open to arguments if I should be lower.)

The crux of my thesis revolves around eight main points:

Point 1: Dordaviprone (ONC201) has been tested in multiple single arm studies in both the front-line and recurrent settings with overall survival results exceeding natural disease history.

Single arm studies are always fraught for misintepretation but I think the matched historical controls above show that there is a decent chance the ONC201 is active both in frontline and recurrent H3 K27M diffuse midline gliomas. Sure, it’s a very tough indication but the separation of the curve and the long tail survival benefit in the n=35 frontline study are intriguing.

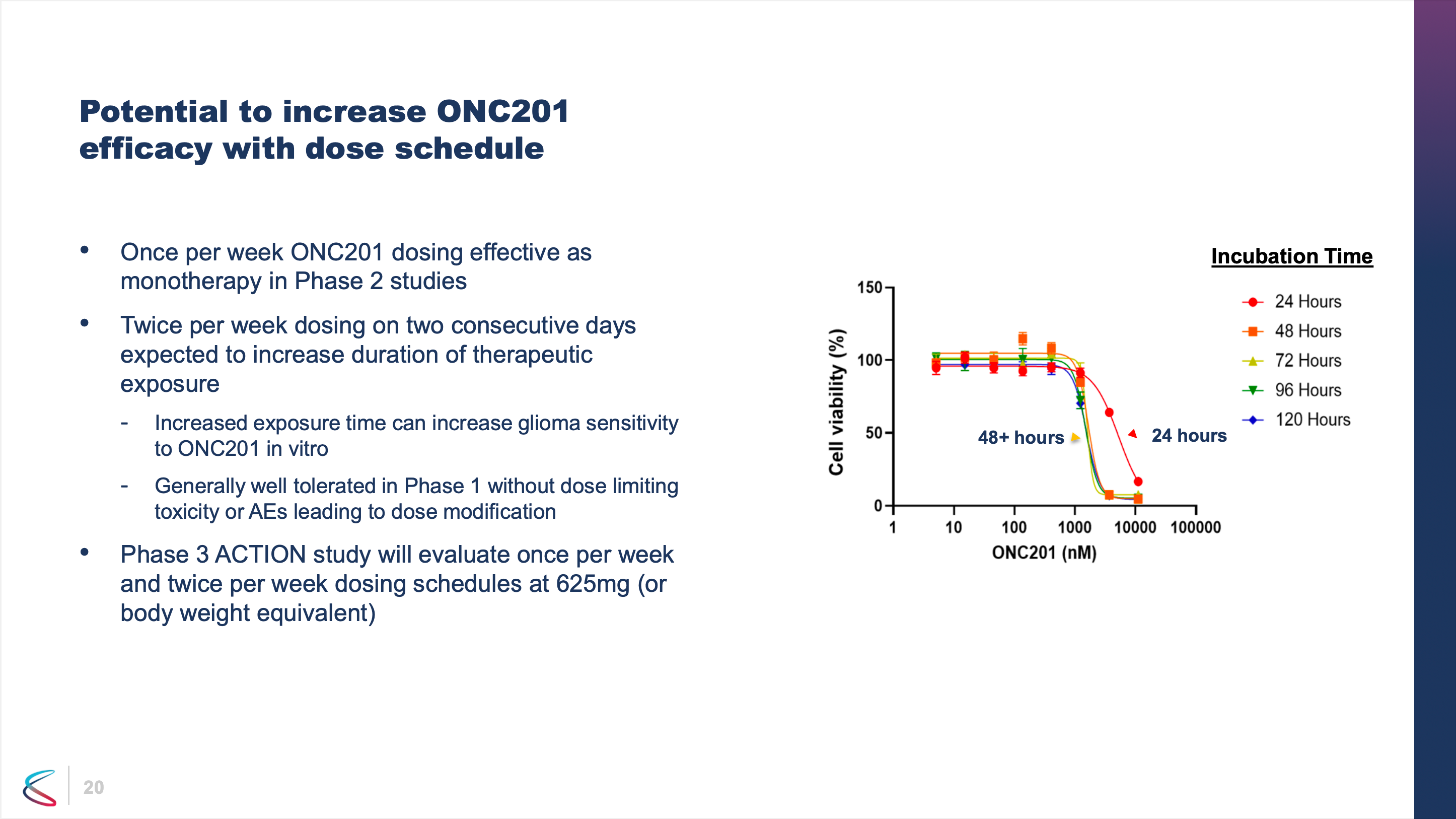

Point 2: The Phase 3 study will have an arm doubling the dosing regimen from Phase 2 due to Project Optimus suggestions and it’s possible the drug was under-dosed in previous studies.

The slide above is from a past deck and not their current slide deck which is curious but it leads me to think that possibly ONC201 was underdosed in past studies and that by doubling the dose (combined with the excellent tolerability profile) perhaps the frontline survival median overall survival could be pushed out to 24 months which would be a doubling of overall survival compared to the n=274 historical control the company published.

Point 3: By running a Phase 3 in the frontline setting, Chimerix has maximized their chances of clinical and commercial success.

Based on the combination of all the Phase 1 and Phase 2 work and investigator sponsored trials, it seems ONC201 works best when given as soon as possible after radiation therapy. So Chimerix has run their Phase 3 trial in frontline H3 K27M DMG. I think this is really the best option from a recruitment angle, a probability of success angle, and a commercialization angle. The trial will have 450 patients randomized 1:1:1 between the dose used in Phase 2, the “doubled” dose mentioned above, and placebo. So there are two independent shots on goal and maybe even a chance to show contribution of effect that increasing the dose increases survival if both active arms hit. The trial seems powered appropriately with multiple interim looks for a chance at an early stoppage.

Point 4: Dordaviprone has repeatedly shown monotherapy activity in at least 20% of recurrent patients with deep responses.

Even in the recurrent setting which is not the best to maximize efficacy, ONC201 showed at least a 20% response rate by very strict RANO HGG criteria and independent review. Between RANO HGG and RANO LGG at least 30% of patients showed a response. Also with a disease control rate greater than 40% it’s possible close to half of patients would experience a survival benefit even if not necessarily strictly being classified as a responder.

Point 5: 2,000 U.S. patients with no approved standard of care could provide peak sales greater than $400m per year at “orphan oncology” pricing, ROW opportunities could add to that or provide non-dilutive capital.

This is a frightening diagnosis with no approved therapies. Achieving 24 months median overall survival would be a big improvement for these patients and an easy commercial value proposition although we still need to do better for these patients beyond ONC201. Two years median survival is just not good enough but it would be a start and encouraging sign given the lack of drug development wins in brain cancer.

Point 6: Dopamine-secreting tumors could provide label expansion opportunities for dordaviprone (ONC201).

ONC201 has shown activity in a very small Cleveland Clinic sponsored trial in paraganglioma with 50% ORR. Would I hang my hat on that going forward as an approvable indication? No. But any signs of activity are encouraging when you have a Phase 3 oncology company trading far below cash. And if the company had profits in the future there would be label expansion possibilities or possibilities for their next generation agent…

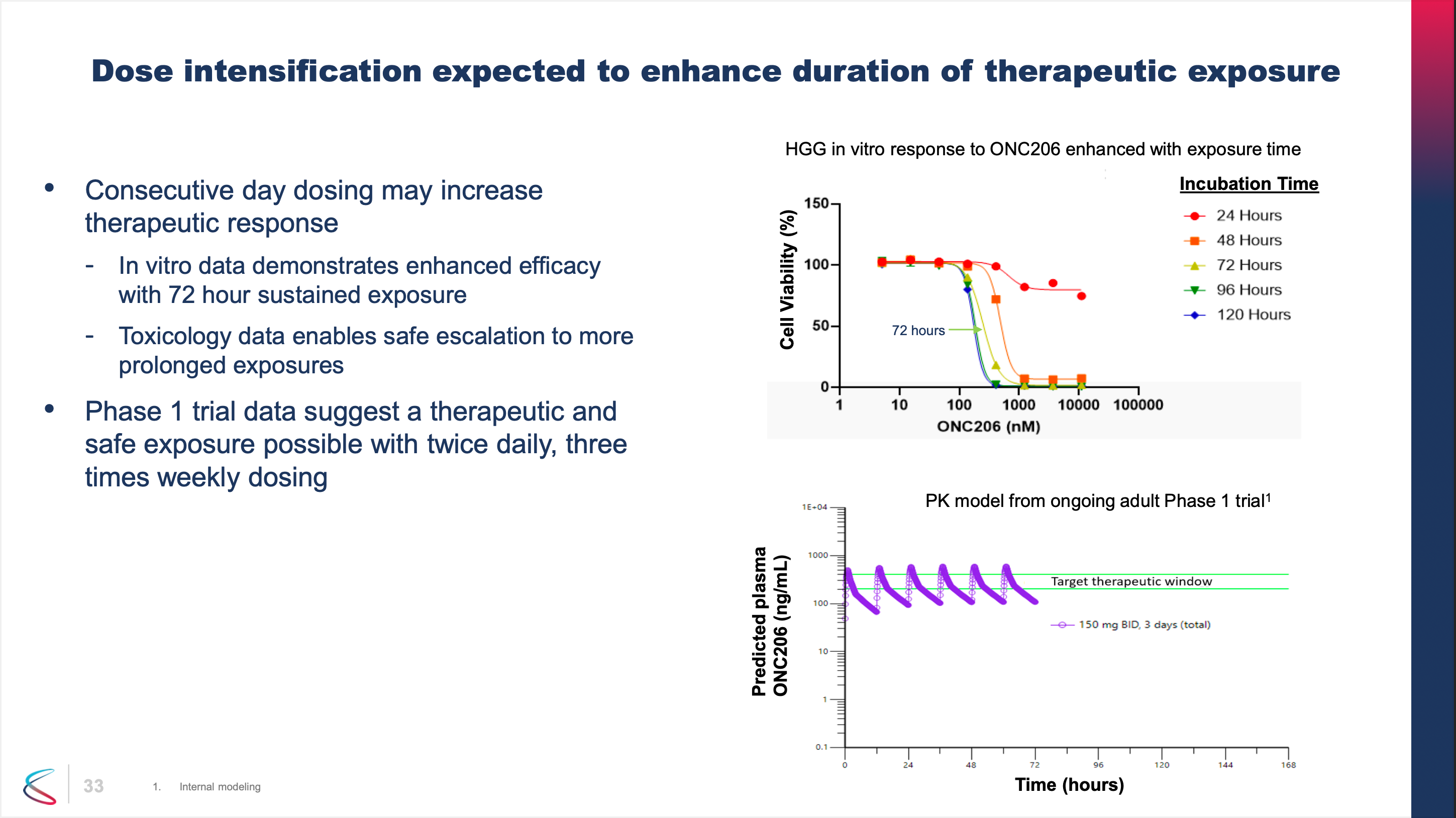

Point 7: A second pipeline candidate, ONC206, is in dose escalation studies looking at tumors outside of the H3 K27M-mutant space.

ONC206 has roughly the same mechanism as ONC201 but is more potent. Chimerix is looking at ONC206 in broader indications. Again, the slide above has been removed from the most recent deck which is puzzling because it shows that if concentrations can be achieved high enough there is preclinical rationale for activity. But since ONC201 has basically negative value, fair to say ONC206 is receiving no value at all. But ONC206 is in a dose escalation study with an update planned for this year so there is a long-shot catalyst in the coming months.

Point 8: The current valuation is not pricing in any further royalties from Emergent Biosciences for their legacy antiviral that was outlicensed.

Chimerix sold Tembexa to Emergent BioSolutions in 2022 and still retains procurement milestone payments and royalties if sales to governments exceed a certain volume. If ONC201 is a complete zero, and if ONC206 is a complete zero, the recovery value of the company and remaining royalty stream might be higher than the market is currently expected, blunting the potential downside of a ONC201 Phase 3 fail, if it were to happen.

In short, I think the floor is higher than the market expects and the ceiling is way higher than the market is currently pricing in. But finding out if I’m right will take a very long time. (Interim data in mid 2025 likely, final readout in mid 2026.)

Hopefully positive enrollment updates and possibly ONC206 data with a response in a non H3 K27M tumor type happen in the near term.

#8: BridgeBio (BBIO) [Last Month: NR, ⭐️]

Keeping it simple on Bridge: Four potential blockbuster drugs including the potential mega blockbuster acoramidis. Tons of data catalysts in 2025 with enrollment updates this year. It’s by far the most expensive market cap on this list but it has the best chance of any clinical stage biotech I know to become a Regeneron-size biotech built from within. You could write 100 pages on this company or one paragraph - I’m choosing a paragraph because that’s all I have time for! I think they have a collection of excellent assets and while the upside might not be as high as other companies on this list I think the risk of ruin is probably the smallest as well. If I were going to recommend one biotech for my “normie” friends who wanted biotech exposure, it might be this one…? The two things you would want for that are a high chance to beat the XBI with lowest chance of wipeout possible so your friends don’t stop talking to you. :-) That’s possibly this although I’m open to other biotech ideas with a diversified and uncorrelated multi-blockbuster pipeline if you have them!

#9: Avadel (AVDL) [Last Month: #7, ⬇️]

Avadel had mostly good news in the past month. A patent lawsuit resulted in a mixed ruling that required the company to pay a very low single digit royalty. This outcome avoided a more disasterous scenario of a very high royalty or injunction against the launch. AFAIK, only one lawsuit remains in the court system and that will start in April. The company won’t comment on legal matters but is giving the outward impression that the LUMRYZ launch will not be affected by any of this. This seems to be the case as of now but I believe in “trust but verify” so I will keep seeing what I can find on the matter from legal consultants. Self-reported launch metrics from the company seem extremely healthy as of now as the company continues to rapidly pick up steam. The only reason I have the position down the list a bit is as the stock has risen it’s a little harder to justify owning versus some of these more pure growth clinical names. There is still multi-bagger potential here though and I want to keep some exposure, especially with a Phase 3 trial in Idiopathic Hypersomnia (IH) starting later this year.

#10: Alpine Immune Sciences (ALPN) [Last Month: #2, ⬇️]

I took this position down a bit this month. And the reason was simple: I reevaluate my positions each month. One day I looked at this stock trading at $39 (that I had bought in the low teens) and had now rallied 200% on essentially a late reaction to data in only six patients total (5 IgAN patients and 1 pMN patient)…I asked myself if holding a stock trading at a $2.7b valuation based on six patients’ worth of data was a Top 5 idea for me right now. I had to concede that it probably wasn’t even if I have huge hopes for povetacicept as a best-in-class dual antagonist of BAFF/APRIL and all the potential indications for which that could be used. This is really more of a reflection of Alpine’s successful last six months and repricing than anything else. The execution seems great; it’s just not as cheap as it once was or as I believe others are currently. I couldn’t kick it out of the Top 10 completely though. Not yet. It very well could double on further updates…the indications are just that large and the comps are very clear based on recent acquisitions. It would be a perfect fit inside a Big Pharma pipeline.

Falling out of the rankings: Coherus (CHRS), Delcath (DCTH), Fusion Pharmaceuticals (FUSN), Glycomimetics (GLYC)

On Coherus, it’s really as simple as I dislike hearing the CEO’s voice on earnings calls by now as well as dislike his excuses for lack of shareholder value creation, a lack of guidance, and questionable strategic decisions plus the fact the story (operating leverage) is taking forever to play out. I’ll probably revisit in May for the call again to see if I feel any kind of optimism but I have pretty much given up hope. There’s value to be had here FOR SURE but their decisions on debt management and divesting a fast growing product make this an exercise in frustration. I challenged them two months ago to prove me wrong - so far they aren’t. But I’ll likely keep paying attention probably because I’m a glutton for punishment. (Just being honest.)

On Delcath, they are activating launch sites, I like the value proposition, but management’s continued preaching of caution and then doing a private placement right before earnings really rubbed me the wrong way. They said they wouldn’t dilute at 4.75 (check the conference presentation February 1), did an offering at 3.75 BEFORE an earnings call, and in general don’t seem to be interested in representing their minority shareholders just the few big shareholders that recapitalized the company. Another watch and wait company now for me, almost solely due to management issues.

On Fusion, acquired by AstraZeneca! A clean win, even if I’m surprised AstraZeneca acquired them before data.

On Glycomimetics, I like it but not enough to crack the Top 10. I don’t have a STRONG expectation that the trial will be successful but see it as a possibility so I view it a bit like gambling. But on an unequivocally successful trial it should be up 500% to 1,000%. On a clear failure it’s basically a zero. Investors seem to want to avoid true binary plays right now especially when you look at something in another disease state like Amylyx in ALS was revealed to be almost completely inert after touting a supposedly successful Phase 2 trial. Just know the risks with this one heading in - you are betting on a low probability, high upside outcome. I said that last month but I have to repeat it because I don’t want anyone dunking on me if this doesn’t work. Also read the disclaimer at the top about not being financial advice, etc. These are my thoughts but you have to form your own on if this binary play makes sense for you.

See you in a month unless something really major happens!

Thanks for reading,

Matt

You nailed $celh!

i think glycomimetics has a high chance of success with uproleselan plus chemo in relapsed and refractory aml.... see the attached seeking alpha article... https://seekingalpha.com/article/4679755-glycomimetics-can-become-game-changer-in-blood-cancers