Xeris Biopharma Is A Dip-Buying Opportunity Ahead Of Accelerating Growth

Recorlev is a growth engine with a large Total Addressable Market on top of a strong foundation with Gvoke and Keveyis, and a potential wild card in a weekly subcutaneous levothryoxine injection.

Word Count: 2,872 words, Reading Time: 14 minutes

Hi everyone, last week I took a much needed week off as I had been publishing 1-2 articles weekly straight since November. After that mini break I’m back refreshed and ready for what I actually think will be a busy time in biotech and the coverage universe I follow. I’m waiting on a couple data readouts (CELC and CRDF) in the next month along with a couple of PDUFA action dates (APLS and REPL) and then we will roll right into earnings reports (EOLS, SCPH, XERS, AVDL, HROW, GERN, TARS, TGTX, etc.)…hopefully it’s non-stop news flow and alpha from here to the end of the year!

Xeris Biopharma XERS 0.00%↑ is a company I have followed in the past but at that time it didn’t really crack my preferred ideas list so I mostly let it languish and fell out of touch with the story. That was my mistake but luckily through divine timing (luck) I have come back in tune with the thesis at the perfect time - recent Q1 2025 quarterly earnings significantly de-risked the company and also the stock is down over 25% from its recent 52 week high providing an extremely appealing opportunity to begin accumulating the stock. Let me explain.

At their recent Q1 2025 earnings call on May 8, 2025, Xeris provided 2025 net revenue guidance. The midpoint of the guidance, $267.5 million, represents 32% YoY growth. I believe the midpoint is very conservative for many reasons:

The company has a history of conservative guidance.

Q1 2025 grew 48% over Q1 2024.

The main growth driver of 2025 revenue, Recorlev, was a focus of their recent investor day and still has a massive Total Addressable Market with extremely minimal penetration.

Recorlev will see a sales force expansion in 2H 2025 which should further accelerate new scripts, the product has a low attrition rate, and it is a maintenance medication which is up-titrated so it should see accelerating revenue from refills in 2025 as well.

Recorlev may also benefit from off-label prescribing in the future as current trends in endocrinology support further testing of cortisol levels in non-Cushing Syndrome indications.

With the current market cap of $696 million, Xeris is currently trading at a Price/Sales ratio of 2.6 based on 2025 guidance which would be a cheap for a company even with low to no growth. But Xeris is a company that had 48% YoY growth last quarter, is guiding for 32% YoY growth across 2025, and most importantly has structural reasons in place why it should grow for the next DECADE based on Recorlev and their pipeline product XP-8121.

But before I do a deep dive into Recorlev and all of Xeris’ growth drivers, let me first touch on Gvoke, which is the product I always associated with Xeris in the past.

Gvoke

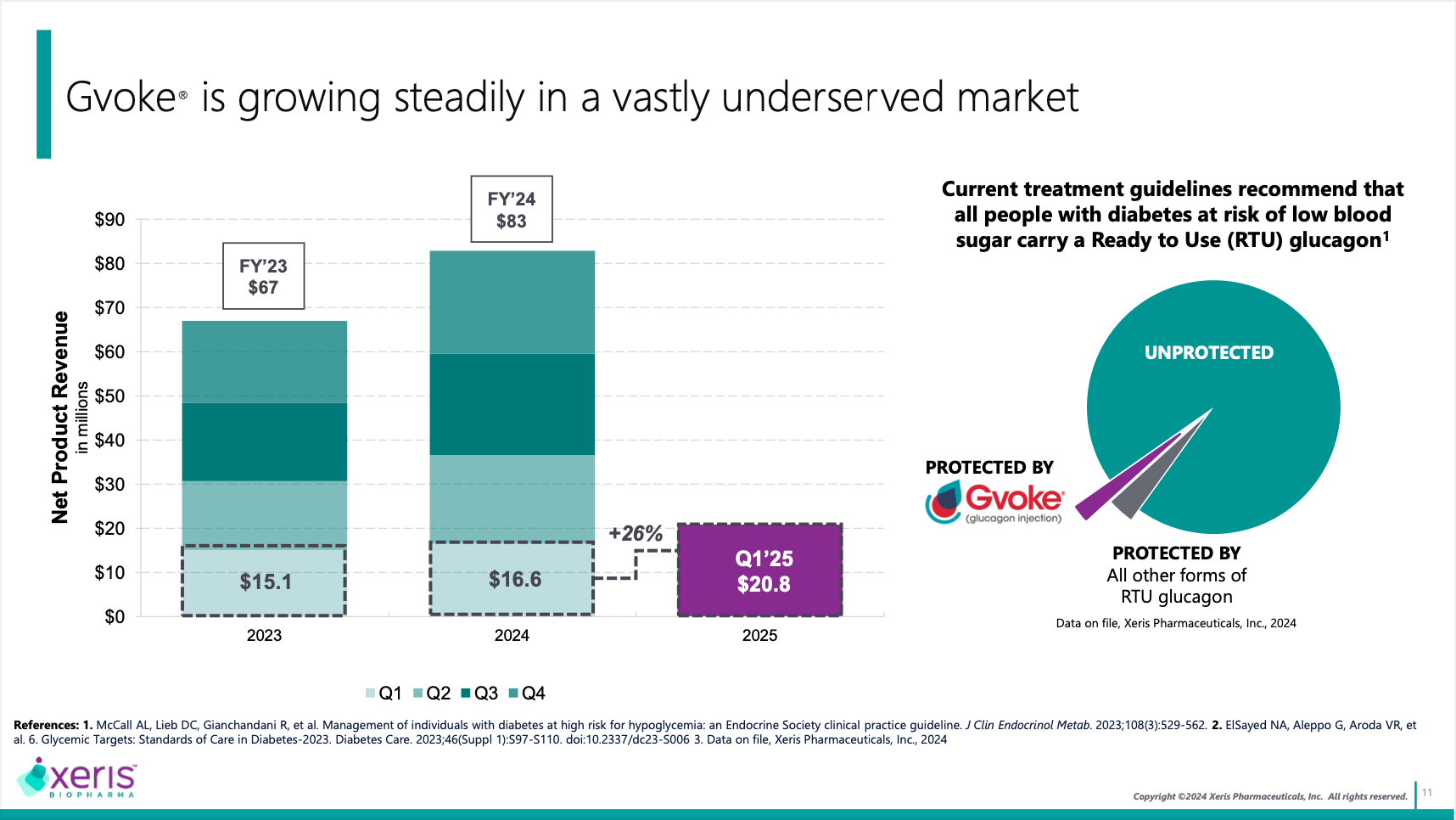

Gvoke is a ready-to-use autoinjector of glucagon for Type 1 diabetics to be used as a rescue medication for extreme low blood sugars and replaces bulky kits that require admixture during a medical crisis. Even at a pricing premium, the value add provided by Gvoke is obvious and its only competition is from a nasally administered glucagon spray. The nasally administered option may be intriguing for some caregivers who are scared about giving injections but I would say most Type 1 diabetics and their close partners and family are very much numb to the idea of giving an injection and the nasally administered option has some fairly harsh after effects. That being said, you could argue how exactly the two newer options will split the market but it’s probably fair to come to the determination there will be roughly a 50/50 split over a very long horizon. However the problem is the market is slow to move off the older kits and the overall market isn’t growing rapidly - every Type 1 diabetic SHOULD have protection at home and school/work at a minimum but sadly the penetration rates are not where they should be even with provider and patient education. Still, Gvoke grew 26% YoY in Q1 2025 - a very solid product that is on track to meet or exceed $100 million in yearly net revenue this year. It’s a foundation to grow from and a backbone for the company.

Recorlev

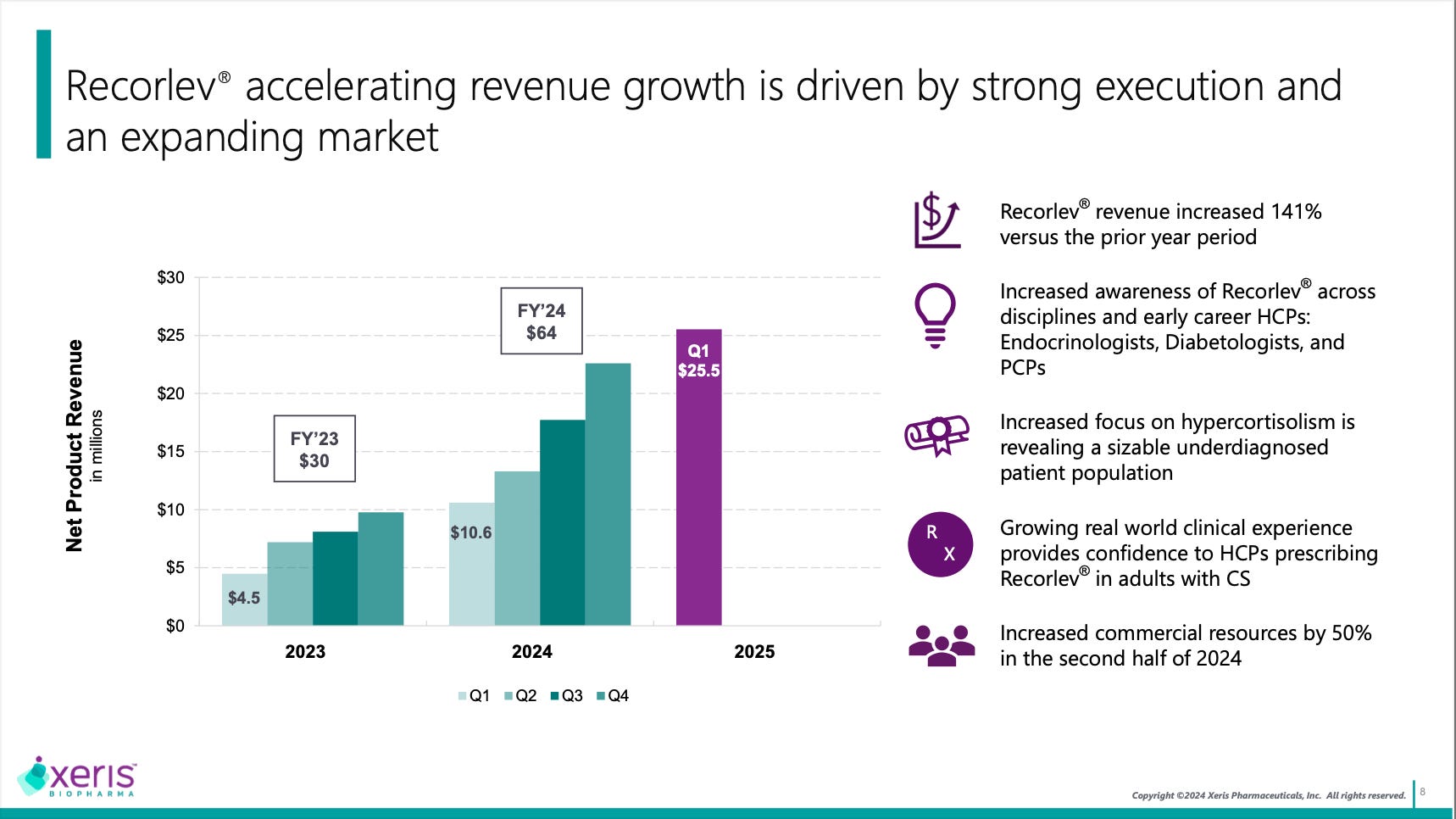

Recorlev’s Q1 2025 revenue number shocked me. In the world of higher-priced specialty medications usually Q1 is flat from the previous Q4 or even slightly down. Recorlev powered through to a new record quarter and the curve of the graph shows accelerating growth. That matches the structural trends on the side of the above slide: increased awareness of the product, greater willingness to treat, and growing real-world data supporting use. After a very slow launch start, Recorlev is now doubling its sales every year and it’s looking like 2025 will continue that trend as I expect net revenue to be greater than $128 million for the product in 2025. But it’s not just the near-term environment that is bullish for the product. There are numerous long-term tailwinds that could make this a blockbuster product and with intellectual property out until 2040, Xeris has time to realize this potential.

The estimates for Overt Cushing’s Syndrome in the U.S. vary widely depending on the source. I have seen prevalence estimates of 7,000 patients…10,000 patients…20,000 patients…26,000 patients. But if we take midpoint at all the estimates we end up with a prevalence of around 15,000 patients in the U.S. conservatively. Recorlev has an annual cost of around $350,000 so the addressable potential is in the billions even if every patient does not receive pharmacological treatment.

First-line treatment includes surgery and radiation but radiation can take years to be fully effective and surgery is not always curative and even patients initially cured can experience relapses later in life. Pharmacological therapy is becoming more of a main-stay as the treatment paradigm evolves in Cushing’s and Recorlev has an argument to be the most comprehensive option to treat the root cause of the disease.

Where other therapeutic options have limitations on use (some only applicable to pitutary-based Cushing’s and others that are only treating hyperglycemia secondary to Cushing’s), steroidogensis inhibitors like Recorlev treat the root cause of the disease. Sustaining cortisol normalization has many positive secondary effects on other comorbidities and, while Recorlev need to be monitored closely for hepatotoxicity, the safety and tolerability profiles are understood and considered manageable given the severity of Cushing’s and lack of treatment options.

At first I was skeptical of Recorlev considering it is just an enantiomer of ketoconazole, an anti-fungal that can be used off-label for Cushing’s, but now I think there is a real case to be made that Recorlev is safer, more effective, and more well-studied than ketoconazole and deserves to be used an as on-label therapy even at a massive pricing premium compared to off-label ketoconazole.

Keep reading with a 7-day free trial

Subscribe to Matt Gamber’s Biotech Newsletter to keep reading this post and get 7 days of free access to the full post archives.