Free Post: My 2025 "No Trades" Model Portfolio

Note: This is the last of my series of posts looking ahead to 2025. This post is 100% completely free for all subscribers. If you enjoy it, please consider a paid subscription.

This publication is 100% supported by readers with absolutely no corporate or hedge fund sponsorship.

(Comparable publications are priced anywhere from 4x to 15x per year my current rates.)

The Portfolio

I’m putting the model portfolio right at the start.

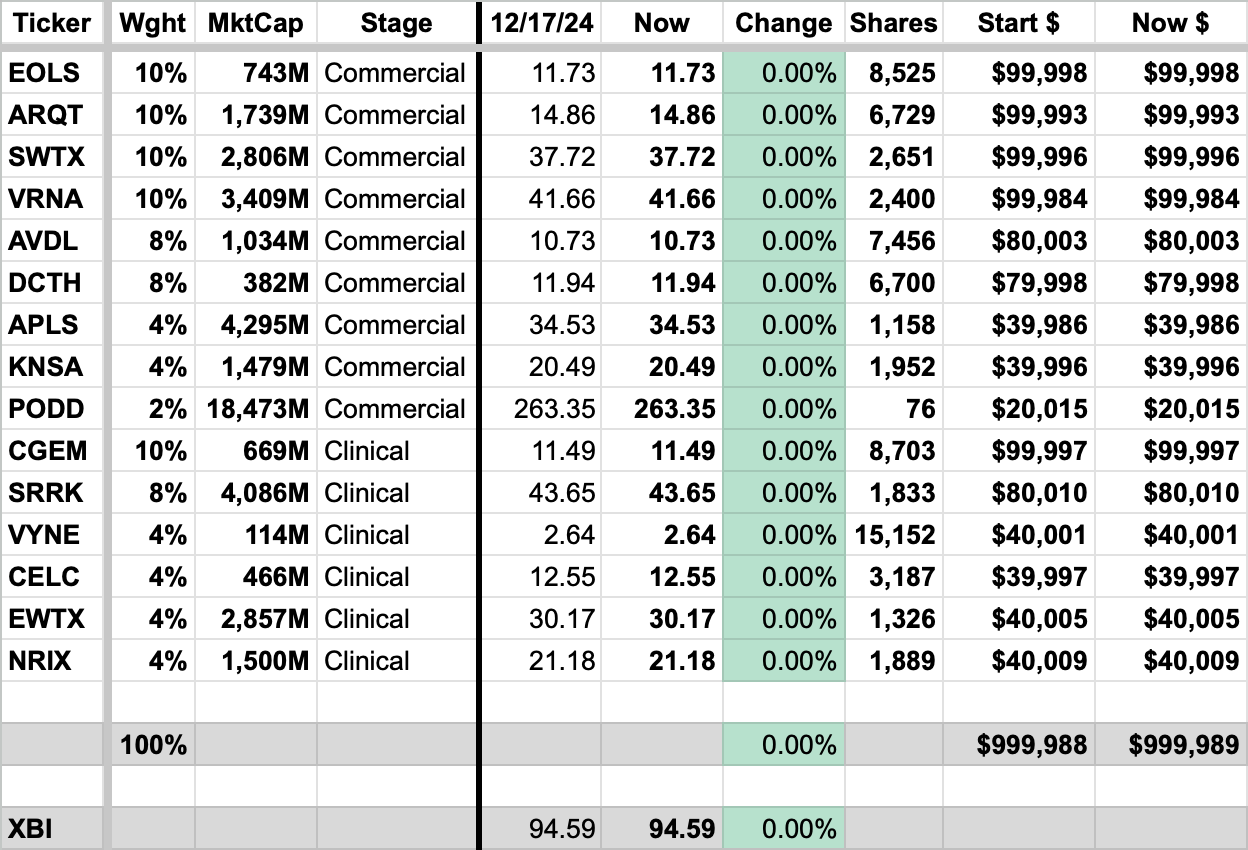

Here’s my best portfolio to beat the XBI benchmark while not making one single trade from December 17, 2024 to December 17, 2025. My goal was to use $1 million as a starting point for the portfolio but I didn’t want any partial shares so the starting point is $999,989.

All prices are as of market close December 17, 2024.

Not investment advice. For entertainment purposes only. I’m not an investment advisor.

The model portfolio is 66% Commercial Stage Biotechs, 34% Clinical Stage.

64% Companies Over $1b Market Cap, 36% Companies Under $1b.

Oncology names comprise 26% of the portfolio. (I’m considering Cullinan an autoimmune disease company as I assume they will sell off their oncology candidates if autoimmune works out.)

The Ideas

Presented in above order. I tried to list what I believe is the bear thesis in italics so I can properly debunk why I believe it is not valid and why I’m an owner of the stock.

The first idea is Evolus (EOLS) which has a FDA-approved neurotoxin (Botox competitor) named JEUVEAU for medical aesthetics and will soon have a differentiated HLA filler line that compliments the neurotoxin line. The bull thesis is the combination of neurotoxins/fillers will eventually be a $10b global market within five years. ($6b neurotoxin, $4b fillers.) This market will be divided up among a few players that have FDA approval and the full line (toxin + filler) for a sales team to utilize rebate-based pricing that incentivizes practices. The most common bear thesis I get pushback with when I suggest to other investors is the toxin isn’t differentiated enough. I would argue two things: 1) third-party research actually argues the toxin is relatively differentiated in terms of time to onset and precision, although I’m not sure how much patients care 2) the true differentiation is in the treatment of the provider! Evolus provides co-branded marketing, a loyalty program, and very slick provider focused software to make providers want to suggest JEUVEAU. In 2025, they will introduce the cold cross-linked filler line which does have meaningful differentiation to the patient (more natural appearance vs. other fills) and gives their sales force more leverage to introduce bundling and deepen provider relationships. The stock is already very cheap and growing at three times (27% YoY vs. 9% YoY) the overall market rate. The company will be profitable this quarter and in 2025.

A company that doesn’t seem to get appreciation despite stacking multiple strong quarters in a row is Arcutis (ARQT). A quick look at what they’ve accomplished in the last few years: three different approvals (ZORYVE 0.3% cream in plaque psoriasis, ZORYVE 0.3% foam in seborrheic dermatitis, ZORYVE 0.15% cream in mild to moderate atopic dermatitis), and soon in May a fourth (ZORYVE 0.3% foam in scalp psoriasis) will launch. I’m not sure what the bear thesis here is…dermatology launches are hard? They are! That’s what makes what has already been accomplished here so impressive. Their first product approval (plaque psoriasis) was the least exciting product-market fit of the four but it has evolved to something that will do over $100 millon annualized soon. Meanwhile the foam has not even been on the market for less than a year and is showing excellent traction and atopic dermatitis saw meaningful sales in less than a full quarter on the market. Moreover, weekly Rx numbers look good and there is a meaningful catalyst in 1H 2025 with the foam approval for scalp psoriasis. (A much more interesting product-market fit than plaque psoriasis.) Perhaps the bear thesis is just raw valuation, but at $1,485 million market cap with the possibility of a blockbuster from both the creams vertical and the foam vertical I feel there is still a lot of headroom here. This is assigning absolutely no value to their research pipeline, as well. They have guided to profitability by early 2026 but I think it could come sooner and management is being prudently cautious.

Another company that has the possibility of multiple blockbuster products is SpringWorks Therapeutics (SWTX). Their launched product OGSIVEO is a systemic treatment for desmoid tumors. The first year launch has been a bit uneven as rare disease launches can be complicated and they also transitioned from a product that was bulk tablets in a bottle to multiple strengths of blister pack NDCs, causing patients to need to get a new prescription. But even with that and a few other challenges, the launch is delivering on the metrics that matter: patient satisfaction is very high, the prescriber base is broadening and deepening with high enthusiasm to use the product more in the 2nd year of launch, and payer receptivity is excellent. Most important of all is the market is larger than the company previously thought with more than 10,000 U.S. patients vs. initial estimates of 5,000 to 7,000 patients. With a list price of $348,000, that upsizing is very meaningful. The bear thesis here is that there will be a competitor product (from IMNM) on the market perhaps in 1H 2027. I think SpringWorks’ rationale for not being worried here is sound: this is a rare disease where most patients will be on therapy by the time the competitor launches, the competitor product will likely have the exact same product profile with less real-world safety data, and patients are very happy with the existing product so switching rate should be low. There won’t be much of a market to launch into if SpringWorks handles their business. SpringWorks might look pricey but they have a second product that will hopefully be approved in 2025 for NF1-associated plexiform neurofibromas, a potential $2b market. So you have a $3.5b market in adult Desmoid Tumors, $2b NF1 for pediatric and adults, plus potential label expansions for OGSIVEO in ovarian granulosa cell tumors, pediatric desmoid tumors, and the rest of the pipeline. I think there is still meaningful upside and the OGSIVEO launch should get them on the path to profitability by the end of 2025.

Verona Pharma (VRNA) at first glance may look expensive for a single product commercial-stage company but it’s really in unprecedented territory as the first inhaled novel mechanism of action FDA approval in more than 20 years. COPD is an insanely large market and of the 8.6 million treated roughly half are still persistently symptomatic despite treatment. 75% of patients have a nebulizer at home and can utilize OHTUVAYRE, Verona’s inhaled PDE3/PDE4 inhibitor. There is an incredibly large patient group out there looking for an add-on therapy that makes them feel better which is exactly what Verona provides. The launch has had an exceptionally strong start and it only takes penetration into roughly ~10% of the persistently symptomatic patients (430,000 U.S patients) to lead to sales over $5 billion/year. Now, the company is not guiding to that number nor am I necessarily expecting it five years from now but even if you take a hatchet to those assumptions there is still an extremely good chance this reaches blockbuster status in the near future. The slope of the launch curve over the next few quarters should make it abundantly clear that this company should be acquired, especially when you look at other possible indications, lifecycle management in progress, and lack of competition in the space. And, hey, I’m not completely ruling out peak sales of $5 billion, either.

Avadel (AVDL) has had some stumbles lately with their Chief Commercial Officer leaving (reasons unclear if he chose to leave or forced out), Jazz Pharma scoring a legal win to (temporarily) block them from entering a second indication when their Phase 3 is complete, and a lower than expected revenue number in Q3 when discontinuations came in higher than expected. All of this news wasn’t exactly fun to read, nor was it good for the stock, but I feel like we have lost the forest from the trees somewhat. (I actually hate that saying - no idea why I just typed it but let’s roll with it.) All of this noise has caused people to forget that Avadel still possesses the only once nightly oxybate for narcolepsy (an approval that was NOT easy to get clinically or legally), their freedom to operate in narcolepsy was recently solidified by a series of court decisions (a lot of risk was removed!), and a new CCO might not be a bad idea to get a fresh set of eyes on why discontinuations increased among the new to oxybate patients, who may need a little more support given that oxybates are a unique class of medicines with risk mitigation, titration, and adverse events that need to have expectations managed. In the end, there are 50,000 patients over the next five years that can be targeted for therapy with Avadel’s LUMRYZ and it has a best-in-class product profile because it doesn’t require patients to wake up in the middle of the night to take their narcolepsy medication. So not only will they attract switch patients but they will broaden the oxybate market by returning patients who previously discontinued back into the fold plus be more enticing for newly diagnosed patients that would otherwise decline therapy. Considering net revenue to the company of $120,000 per patient once titrated up and it’s easy to see the potential market size here. At a market cap of $1 billion, and with the company already achieving profitability, it’s not hard to make the numbers work even if the company hits a couple more stumbling blocks along the way.

One of the greater biotech redemption stories of the past few years is Delcath (DCTH) and their targeted high-dose chemotherapy product for metastatic uveal melanoma. Once left for dead due to safety issues of the first generation filter and regulatory issues, new management and fresh capital turned the story around from near zero with a Gen 2 safety filter and fresh passion for the potential of the HEPZATO KIT. The company is already close to profitability and the only thing really keeping a lid on the stock is the slower pace of rollout for new treating centers. A complicated product like this requires a lot of training and site-specific approvals and the company has lagged even its initial conservative estimates. Currently, 13 centers are treating with another four accepting referrals so will likely start treating soon. The good news for the company is they really only need 25-30 centers treating to unlock more than half of the $600 million total addressable market. A big catalyst for the company, aside from continuing to activate centers, is a trial readout of HEPZATO KIT in combination with immunotherapy vs HEPZATO KIT alone. If they can show synergy with immunotherapy they can be sequenced earlier in therapy and get to peak sales much faster which will throw off cash allowing them to fund Phase 2 trials in many different oncology indications. Considering their still reasonable market cap under $500 million even with recent warrant exercises (which also provided capital), Delcath is reasonably priced for growth ahead with major upside on new data, continued execution, or the possibility of an acquisition given the specialized medtech niche in which they sit.

I talked a lot about Apellis (APLS) and therapeutic area of Geographic Atrophy in my 2025 Biotech Investing Preview last week. I don’t need to re-type all of that (I’d encourage you to read it!) but only to say the bear claim that the Geographic Atrophy launch has peaked is greatly exaggerated, IMO. Apellis, even though it’s the second most expensive company on the list, is intriguing because I still have faith that SYFOVRE for Geographic Atrophy can be a $2 billion to $3 billion product and that EMPAVELI for C3G / IC-MPGN can also be a blockbuster product. I also think once these dynamics become most obvious it’s also a very logical acquisition target, although I never invest for that possibility. In spite of a spate of good news (the C3G/IC-MPGN Phase 3 data, bad news for GA competitor Astellas regarding label expansion, fairly strong underlying QoQ vial growth last quarter and new start market share) Apellis is in a period of strong negativity that is probably a buyable dip.

Another stock that is well off the highs on some execution concerns is Kiniksa Pharmaceuticals (KNSA). Namely their last quarter revenue for their Recurrent Pericarditis drug ARCALYST came in a little light QoQ considering they have a $3.5 billion dollar addressable market (14,000 target patients with multiple recurrances x $250,000 annual cost) from which to find patients. The stock had posting some great growth before so we will see if it’s just a one quarter hiccup. The bear thesis is that they have to split profits 50/50 with Regeneron so they will never be acquired and also the pipeline is pretty light. Even if you assume the pipeline is a zero, they will never be acquired, and accounting for the 50/50 profit split the company seems pretty cheap just on a pure valuation basis, especially in light of likely IP protection until the late 2030s and little competition in the near-term.

The last and smallest allocation of the commercial names is Insulet (PODD). At a $19 billion valuation, I wouldn’t blame anyone skipping them. It’s somewhat of a sentimental pick for me but I maintain they have they have a total addressable market of over $20 billion with little competition. But this company profile doesn’t really fit with the others on the list, but evangelism of the OMNIPOD 5 is somewhat of a personal passion for me.

I continue to think Cullinan Therapeutics (CGEM) is the most attractive of the clinical-stage names. It’s massive cash pile gives it a lot of cushion for safety but the potential upside of their candidate CLN-978 is enormous. The SLE data in Q4 2025 is a major defining moment for the company and gives them a chance to establish a best-in-class efficacy with an actual scalable modality in this large population with a big unmet need. Yes, I know CD19 is insanely insanely crowded, but I like CGEM the best.

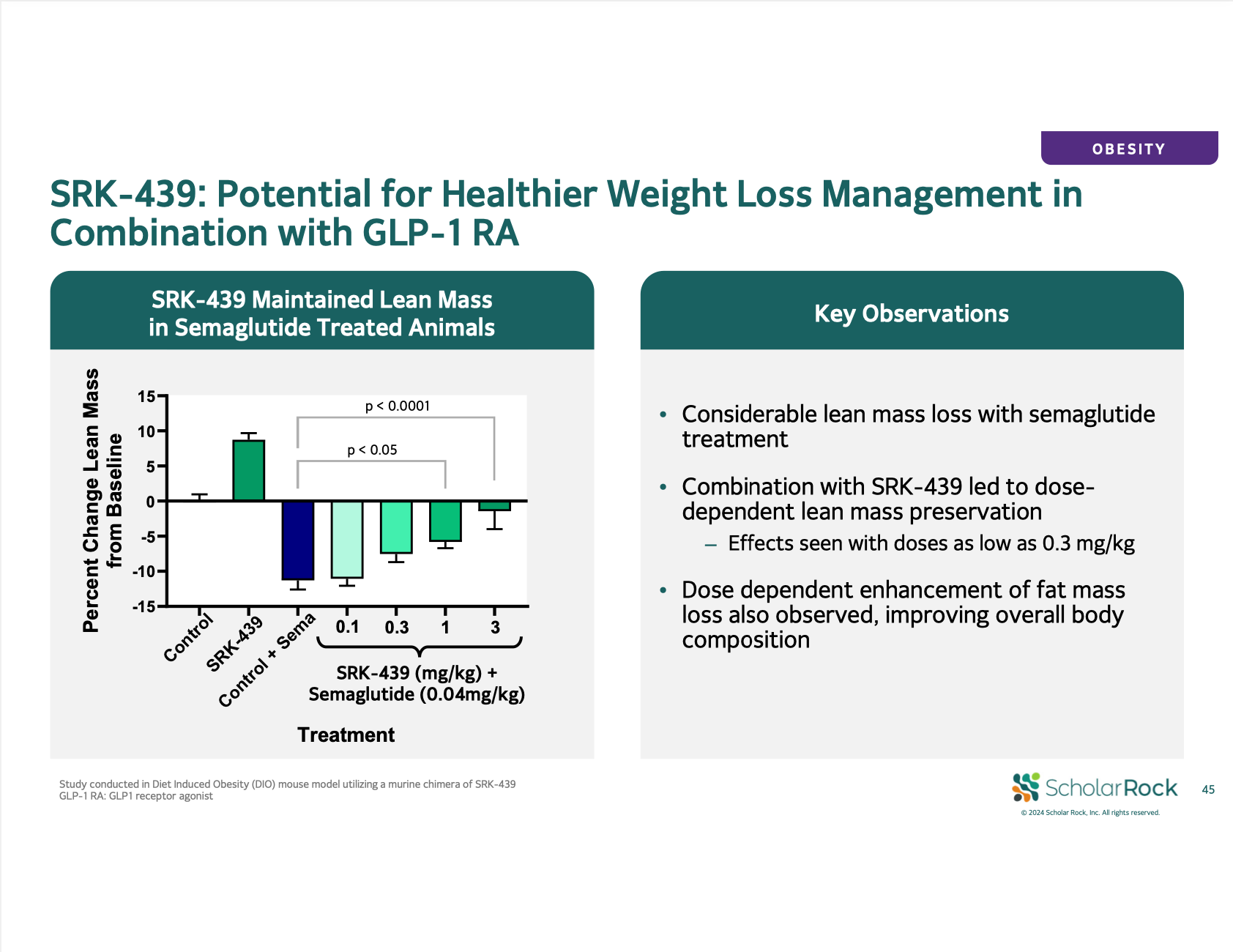

Another clinical-stage company that enjoys an unusually large margin of safety is Scholar Rock (SRRK). Their Phase 3 data for SMA is already in and was surprisingly strong given the uncertainty heading into the readout. Barring some unforseen black swan type of news the drug should be approved and be a blockbuster as an add-on to existing SMA treatments. Normally I would never own a company in the 14-18 months between Phase 3 data and approval (six months to file for approval, two months to get application accepted, six to ten months for review depending on review status) but in this case there is a meaningful data set in the meantime. Their candidate SRK-439 being tested as an add-on therapy in obesity to preserve lean mass will have a substantial proof-of-concept readout. I think most reading know obesity is bar none the most sought after therpeutic area right now. Even though bears might insist Scholar Rock is already a large company in market cap for a clinical-stage company, a strongly differentiated add-on obesity asset would surely meaningfully inflect value for the company and make it a strong acquisition target. Although you can never take too much from the pre-clinical data, it looks good. They already have a history of pulling one rabbit out of their hat when the market wasn’t giving them much credit.

I’m really interested to see what’s in store for Vyne Therapeutics (VYNE) in 2025. Aaron Rosenblum has been all over the story and I’m not sure how much unique I have to add aside but I too am encouraged by the investigator excitement for VYN201, potential best-in-class product profile, and it is the cheapest valuation in my portfolio as well. Bears might say the vitiligo Phase 1b was only a 29 person dose-ranging trial but there was clear dose response between the three doses, efficacy results better than SoC therapies in a disease with low placebo response, and the Phase 1b trial looked only active disease patients which are the hardest to treat. And then aside from VYN201 (the topical product) you also have a pretty neat kicker of VYN202 which is a systemic selective BET inhibitor that has the potential to be used in a host of indications. They probably need -201 to be successful for continued access to funding but it’s a nice bonus for investors who plan to be long-term holders of the stock.

One of the more binary and scary names to hold is Celcuity (CELC) but I wanted to include it because the upside is so immense. I wrote a lot about Celcuity in my 2025 preview and don’t have too much to add aside from the company will have two company-defining readouts for their PI3K/mTOR inhibitor gedatolisib in 2025. I tried to avoid names where I’m “betting the farm” on Phase 3 data but with a 4% allocation I think I have enough safety elsewhere in the portfolio to take a small risk. The bear thesis here, aside from competition, is that there was no placebo-controlled data in Phase 2 and instead a bunch of single-arm dose expansion cohorts with a mix of baseline characteristics, different mutation statues, varied prior therapies and staged disease. Still, I feel Arm D most closely matches what would be seen in the Phase 3 trial and if the data repeats would be strongly considered to be standard-of-care in 2L HR+/HER2- advanced breast cancer.

A clinical-stage play I like a lot because they have two separate, completely uncorrelated “shots on goal” is Edgewise Therapeutics (EWTX). This is another name that was mentioned in the 2025 preview when I was talking about cardiac myopathies. Edgewise will be providing plenty of new data in 2025 on their cardiac myopathy program EDG-7500 which may serve as proof-of-concept depending on how high your burden of proof is based on Cytokinetics setting the bar with some pretty solid Phase 3 data. I know there are still a lot of skeptics on the cardiac myopathy program thinking that the improvements EDG-7500 could offer over the CYTK drug are insignificant. In 2025, Edgewise will have a chance to further poke holes in that theory. Also in 2025 their Becker Muscular Dystrophy drug sevasemten will have regulatory updates related to the data they released two days ago. It’s unclear as of now whether the FDA will let them file for Accelerated Approval based on the data (I saw one poll that was split roughly 50/50) but the stock is only up roughly 10% on a dataset that I felt was overall mostly positive so there is certainly room for the stock to run higher if the FDA is accommodating to getting them on the market 18 months earlier than originally planned.

The last company on the list is Nurix Therapeutics (NRIX). I didn’t originally have Nurix on here but the valuation has come in to a reasonable level. They do have competition from Beigene but I view their BTK degrader NX-5948 as basically equal with Beigene’s and on roughly the same timeline. I think those two will divide the mega-blockbuster opportunity to replace BTK inhibitors with a more potent drug with less resistance mutation liabilities. The market is so massive that even a 50/50 split would make Nurix a huge winner…not to mention the optionality of other drugs built on their platform. For that reason, I also think the company is highly likely to be acquired in the coming years. It seems like a pretty great fit for a Big Pharma.

First Stock Out: Tyra Biosciences (TYRA)

I’m always curious in the NCAA Basketball Tournament (or now the College Football Playoff) who is the team closest to making the cut but ultimately missing out. For me when making this list, it was Tyra Biosciences. I love the idea of FGFR3 inhibition for skeletal dysplasias but BridgeBio has a pretty large head start on them and Tyra isn’t exactly moving at a lightning speed. But most importantly: what I said earlier about SpringWorks not worrying about competition (no differentiation, high patient satisfaction, most patients already on therapy, 3 to 5 years late to market) would unfortunately also apply to BridgeBio/Tyra in this disease space. Even though Tyra might have a more selective agent unless they can meaningfully differentiate from BridgeBio on efficacy (safety would be near impossible) then why would a patient would honestly be interested in switching? I love the idea of a pure play on FGFR3 but even in a potential $5 billion market you need to have a value proposition if you are late to market. (Also, Alabama can’t lose to Oklahoma by three touchdowns.)

If you read all the way to the end, you are clearly one of my most loyal readers and I’m so so grateful for you. If you wouldn’t mind would you share this post on social media or with a friend since it is completely free?

Happy Holidays, Happy New Year, and Go Devils in the College Football Playoff!

Best wishes and thank you to my paid subscribers for making this possible,

Matt